Table of Contents

Navigating the Shifting Landscape of Mortgage Lending

Over the past few years, mortgage lenders have faced a relentless tide of change. The once-booming refinance market has cooled significantly, and purchase volumes have dropped amid skyrocketing home prices and tightening credit conditions. According to the Mortgage Bankers Association, mortgage loan application volume dropped by more than 60% between early 2022 and late 2023, hitting its lowest level in over two decades. Meanwhile, data from Scotsman Guide shows that total mortgage originations in the U.S. fell to $1.5 trillion in 2023, a sharp decline from $4.4 trillion in 2021.

This downturn can be attributed to a combination of high interest rates, elevated home prices, and inflationary pressures—all of which have put pressure on household budgets. With the average 30-year fixed mortgage rate reaching 7.79% in October 2023, affordability has taken a major hit. Consumers are spending less, saving more cautiously, and rethinking homeownership timelines altogether.

Borrowers today expect personalized, digital-first experiences, and lenders are under pressure to deliver. Traditional models are being challenged not just by economic headwinds, but by the rapid rise of fintech competitors offering faster, more flexible loan options. As we step further into 2025, staying competitive means doing more than riding out the storm. It means investing in smarter technology, recalibrating business models, and preparing for what comes next.

“Mortgage lenders that embrace automation and AI are not just surviving—they’re gaining ground in a volatile market.”

The Last Three Years: A Market Under Pressure

The U.S. housing and mortgage markets have been defined by instability since 2022. The combined impact of inflation, rate hikes, and constrained supply has shifted the dynamics for both buyers and lenders.

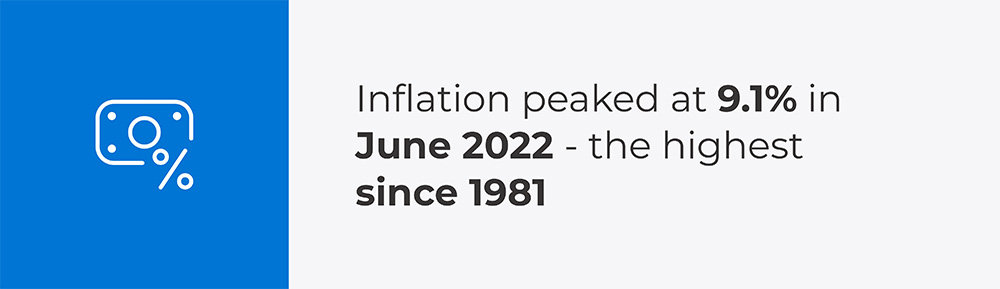

- Inflationary Pressures: Inflation reached a 40-year high in mid-2022, driving up the cost of living and reducing borrowers’ disposable income. This directly impacted their ability to qualify for mortgages or save for down payments.

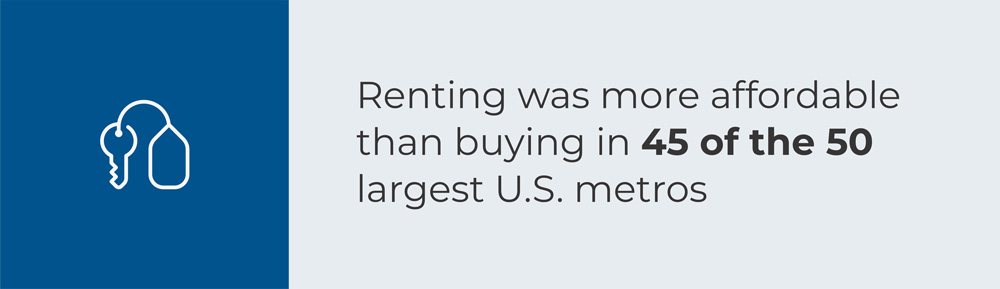

- Skyrocketing Home Prices: Despite cooling demand, limited inventory kept prices climbing. Affordability hit a 38-year low, according to federal data.

- Limited Inventory & Institutional Buyers: Housing supply remained below pre-pandemic levels. Simultaneously, institutional investors purchased a growing share of available homes, intensifying competition and pricing out average buyers.

2025 and Beyond: Where We Stand Now

With interest rate hikes slowing but regulatory and economic pressures mounting, lenders are in uncharted territory.

Policy Uncertainty Takes Center Stage

Changes in GSE policies, new Basel III capital requirements, and state-level legislation are keeping compliance teams on high alert.

Economic Headwinds Are Real

Beyond policy, a cocktail of indirect factors—tariffs, consumer sentiment, affordability, and a looming recession—are creating operational strain.

Originators and Servicers Both Feel the Squeeze

Origination volumes are low, while servicers face increased scrutiny around compliance and foreclosure prevention.

What Lenders Must Do to Stay Competitive

Survival is no longer the goal, sustainable growth and digital resilience are. Here’s how forward-thinking lenders can prepare for the road ahead:

- Catch Up on Automation

Legacy processes are a liability. Streamlining loan origination, underwriting, and servicing workflows is no longer optional. Take the window of opportunity of lower origination volumes to reengineer your process and apply the automations available to your disposal, e.g., API-fication, RPA, IPA, APA to name a few. - Adopt AI with Intention

From underwriting to customer service, AI is becoming embedded in mortgage workflows. But success depends on using the right model for the right tasks, a well-trained chatbot in NLP with the foundational technology of combined ML and LLM can perform wide range of uninterrupted activities across origination and servicing, read Agentic AI. - Build a Modern Foundation

Transitioning to cloud-native infrastructure and modular tech stacks enables faster adaptation to market demands. Be ready for the next wave by adopting the best-in-class cloud technologies bringing in scale, efficiency, and business continuity. - Lean on Predictive Intelligence

Predictive analytics helps lenders proactively manage risk and forecast business growth. From propensity to close, likely to refi, default prediction, today’s LLM powered ML models can help lenders stay ahead of the curve. - Leverage GenAI for Operational Scale

From document automation to borrower interaction, generative AI will be a game-changer. Gen AI’s automation boost is going to be a differentiator for lenders adopting them early and driving down the origination time and cost. - Focus on Retention and Experience

Customer loyalty is a growth strategy. Hyper-personalized experiences and retention programs can drive revenue. High borrower satisfaction in servicing portfolio can reduce the borrower acquisition cost in the origination portfolio. Investment in high end digital experience for borrowers have high multiples of ROI. - Double Down on Compliance and QC

With regulators ramping up enforcement, robust compliance frameworks are a must-have. Changes to policies, regulations/deregulations give rise to compliance needs required to prevent frauds and protect borrowers, lenders, and investors. Lenders must be ready with decoupled business architecture that allows for prompt implementation of the new regulations.

Final Thoughts

Mortgage lending has always been cyclical. But the velocity of change today demands a more agile, technology-forward approach. Whether you’re an originator looking to modernize workflows or a servicer striving to protect existing portfolios, now is the time to act. By embracing automation, AI, and data-driven decision-making, lenders can not only weather the storm – but lead through it.

Roy, VP of Enterprise Solutions, is an accomplished technology and business leader, with 25 years of experience in helping clients across different industry verticals solve business problems through technology adoptions. In this role, Roy sets the strategic direction of the business unit, promotes Speridian’s client-first culture and focuses on creating sustainable growth by bringing together the industry’s leading technology trends, capabilities, solutions, partnerships, and subject matter expertise into a single integrated unit. Beyond his practical vision on business modernization Roy works closely with Speridian clients to gain business advantage from large-scale digital transformation programs.

Insights on Speridian Technologies’ Lending and Mortgage Solutions