7 Reasons to be Prepared for Increased Delinquency in 2021

As the economic uncertainties from coronavirus continues to roil the financial sector, mortgage investors, lenders, and servicers are bracing for increased levels of delinquency, forbearance, and defaults. Eventual recovery is expected but applying predictive analytics to your mortgage portfolios right now will mitigate significant losses in the coming months and years. No matter what your exposure in the mortgage market is, there are plenty of signs that a downward trend will endure for several quarters. Here are the top 7 reasons to expect the worst.

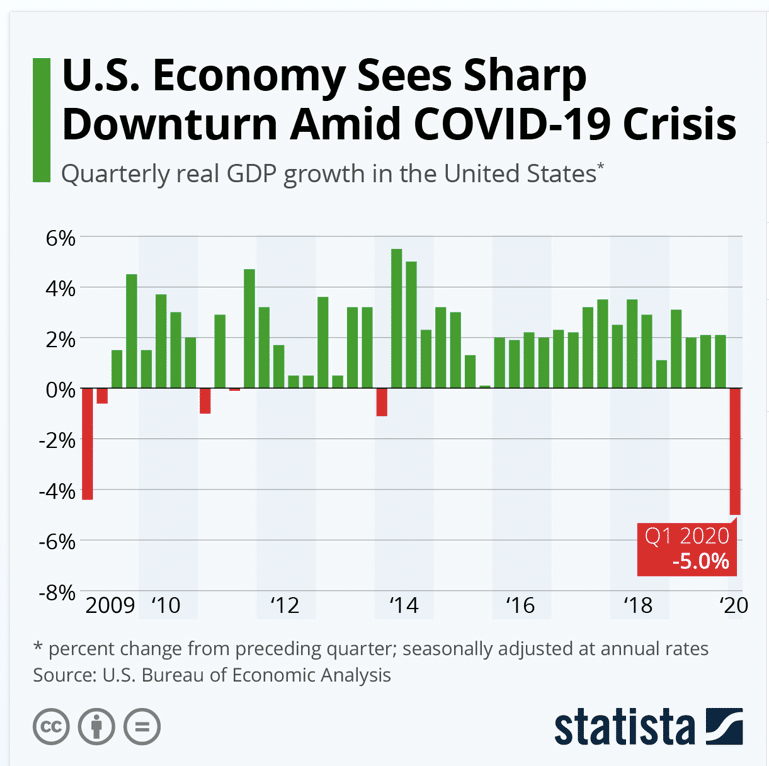

Reason 1: Covid-19 is expected to contract the US economy twice as much as the Great Recession in 2008-2009.

Representing the largest shock to the U.S. economy since 1947, Covid-19 is forecast to result in the contraction of activity to reach -30% Q-o-Q annualized in Q2 2020, representing two times the cumulative contraction of 2008-2009.

Reason 2: Covid-19 is forecasted to increase US delinquency rate by 6.5% and insolvencies by 25% in 2020

Fitch foresees the majority of impacts landing in 2021, as several sectors that experienced complete or partial shutdowns, including restaurants, casinos, movie theatres, airlines, hotels, gyms and non-food retailers are at high risk of default. The rate could top 7% this year without liquidity relief.

Reason 3: Delinquencies are Uncomfortably High

In April 2020, 6.1% of mortgages were delinquent by at least 30 days or more, the nation’s highest overall delinquency rate since January 2016. Serious delinquency rate – defined as 90 days or more past due, including loans in foreclosure – increased to 4.1% in July up from 1.3% a year earlier. July’s number represented the highest rate since April 2014. All of this spells trouble for a flagging market.

Reason 4: The 30-day transition rate is at its highest since 1999

For context, in January 2007 (before the financial crisis) the 30-day transition rate was 1.2% and peaked in November 2008 at 2%. The share of mortgages that transitioned from current to 30-days past due jumped to 3.4% in April 2020, up from 0.7% in April 2019 – the highest transition rate since January 1999.

Reason 5: 6.8% of all active mortgages, representing $751 billion in unpaid principal, are currently in forbearance.

In early September, around three-quarters of the 3.7M mortgage holders in forbearance —who have been delaying their payments and sinking deeper into debt— renewed, extending their forbearance by another three months. As of sept 29, roughly 3.6 million homeowners remain in pandemic-related forbearance plans. When their forbearance terms come to an end, expect a hike in defaults.

Reason 6: An L-shaped recovery is looking more likely as stimulus bills stagnate.

A report published in April projected a worst-case scenario where the COVID-19 crisis extended beyond two months, resulting in an L-shaped recovery (as opposed to the more optimistic U-shaped recovery) with cumulative GDP losses 6 times greater than the subprime crisis in 2008. This will send the economy at-large into a contraction and possibly even a recession, inevitably impacting the mortgage market.

Table of Contents

66%

of U.S. cities where renting is more affordable than buying

36.6%

of American households who rent;

a 50-year high

650

The average renter’s credit score

74.4%

of rental units are owned by investors

24%

of rentals currently at risk of default

Reason 7: There are still many high-risk loans whose forbearance will expire in the next six months

Government and private sector forbearance programs allow borrowers to delay their monthly payments for at least three months and for up to a year. Forbearance is granted in three-month terms, and so far more than 75% of borrowers in bailouts are on extensions since March. As large numbers of mortgage holders exit their forbearance periods, many may still be unable to service their loans.

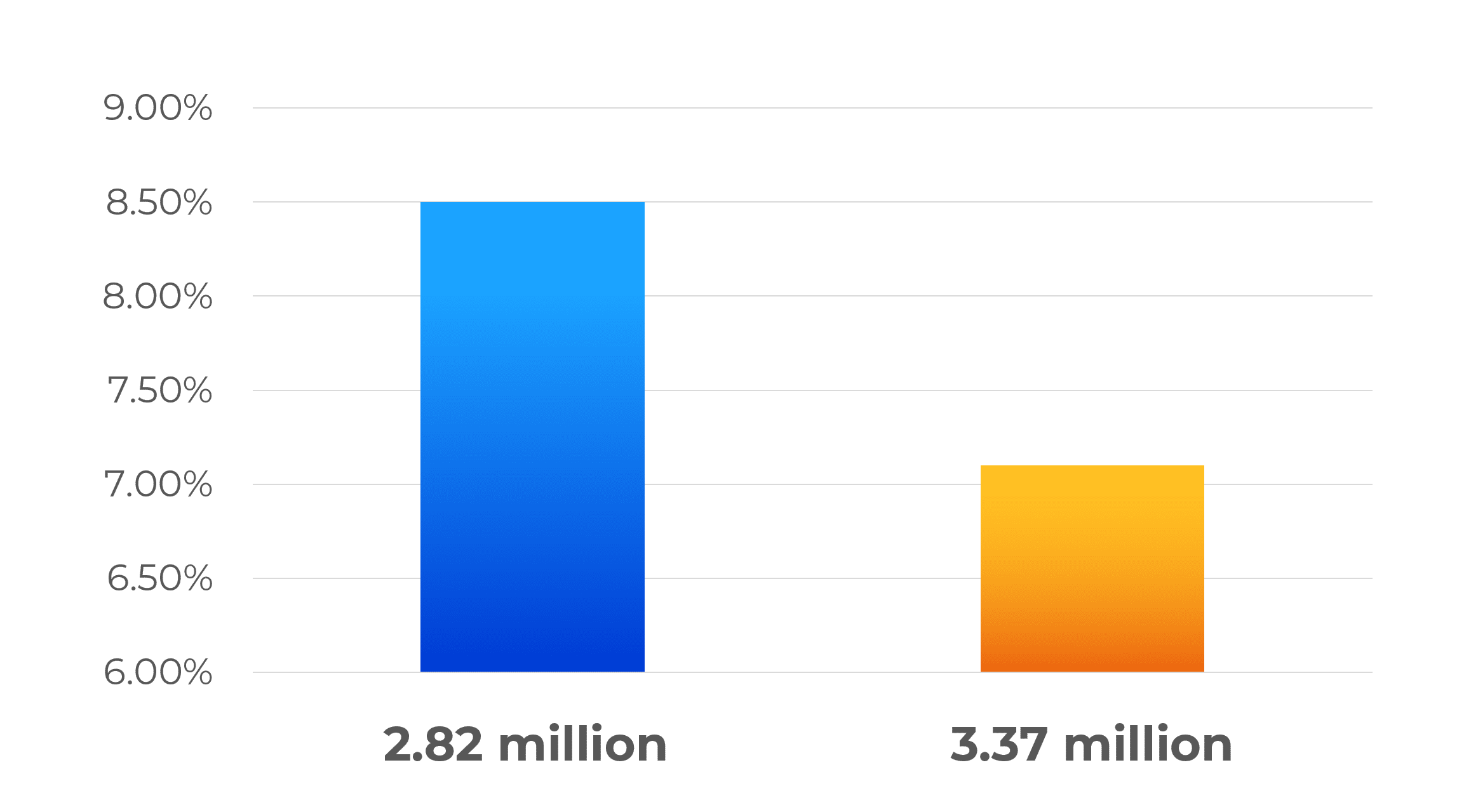

In September, 8.5% of renters, or 2.82 million households, missed, delayed or made a reduced payment while 7.1%, or 3.37 million homeowners, missed their mortgage payment.

Conclusion

Despite grim current forecasts in the mortgage market, a solution designed to help minimize losses already exists. Using machine learning, Speridian’s Delinkure solution can help minimize losses and protect portfolios quickly and easily. Reach out to a representative today for a Delinkure demo to see how you can protect your assets with one simple product and keep homeowners in their homes.